global_02 フィルダコラム

インドネシア農村部の零細起業家としての女性のエンパワーメント

日本語

インドネシア農村部の零細 起業家としての女性のエンパワーメント

シェアリングエコノミーは、情報通信技術の発展から生まれた製品の1つです。

コミュニティは、経済ベースのサービスの共有に積極的に反応しました。シェアリングエコノミーは、商品、車両、または財産を共有することだけではありません。必要な資金を調達するのに役立つ人々とプラットフォーム間の直接貸付を含む、金融を適用する共有経済もあります。

それらに潜在的に興味を持っている人々の間で新しいアイデアの開発を目的としています。

インドネシアで金融を実施するシェアリングエコノミープラットフォームの1つは「Amartha」です。

Amarthaは、投資家を農村地域の女性の超零細および零細企業に接続するピアツーピア「P2P」融資会社です。ベンチャーキャピタルを必要とするビジネスアクターは、個人または機関であるAmartha投資家から資本を得ることができます。

資金を貸し出す投資家には、プロバイダー、この場合はAmarthaが提供するクレジットスコアリングシステムに基づいた特典が提供されます。

Amarthaは、運転資金の融資と農村地域の女性の零細起業家のエンパワーメントに焦点を当てた、ピアツーピアの融資金融テクノロジー「fintech」のパイオニアです。

Amarthaは、オンラインとオフラインの活動を組み合わせて、covid-19パンデミック時にAmarthaパートナーの生産性を維持する戦略を実装しています。

オンラインとオフラインの組み合わせにより、Amarthaは、パートナーの福祉のためにさまざまな製品イノベーションを提供するなど、テクノロジーの使用を最適化します。

その1つは、A +「Amartha Plus」アプリケーションを介して行われ、Warung Loan(小さなお店ローン)、などのさまざまなサービスから卸売りショッピングまでを容易にします。資金調達へのアクセスを提供することは別として、女性の零細起業家に力を与えるオフラインまたはフィールド戦略。Amarthaはまた、ビジネスオルタナティブトレーニング、無料のヘルスチェックのための金融リテラシートレーニングなどの定期的な支援とトレーニングを提供しています。

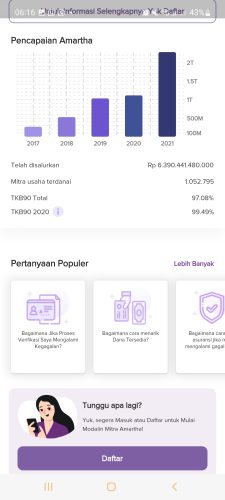

Amarthaは、農村地域で金融サービスを利用できない零細起業家に資金を提供しています。Amarthaが選んだビジネスパートナーは、150万ルピアからの自己資本要件を持つ女性の零細起業家です。

将来のローン受領者の選択プロセスは、クレジットスコアアルゴリズムを使用して実行され、ビジネスおよびパーソナリティ分析に基づいて適格性を評価します。

Amarthaを通じて資金調達をしたい投資家として、アマルサはグループ資金調達システムを適用して相互協力の精神を強化しているため、心配する必要はありません。

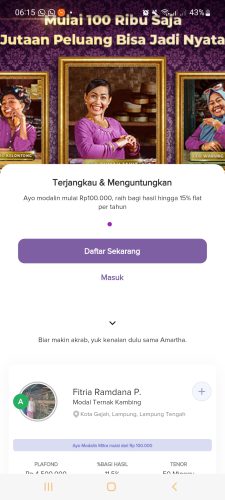

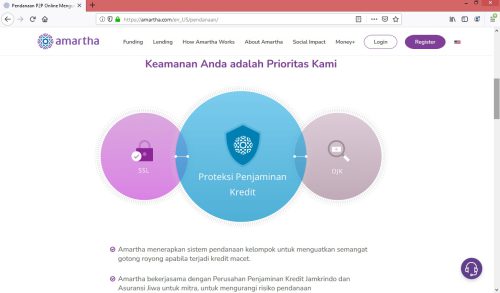

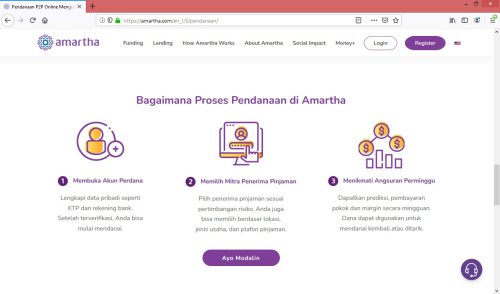

Amarthaは、金融サービス庁(OJK)を通じて政府によって登録および監督されています。資金調達プロセスは簡単です。最初に貸し手アカウントを開きます。 次に、ローンの受取人のパートナーを選択します。場所、業種、ローンの上限に基づいて選択することもできます。次に、毎週の予測、元本および証拠金の支払いを受け取ります。 受け取った資金は、借り換えや引き出しに使用できます。

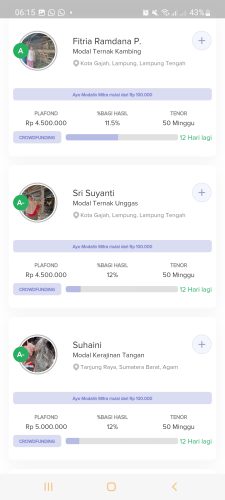

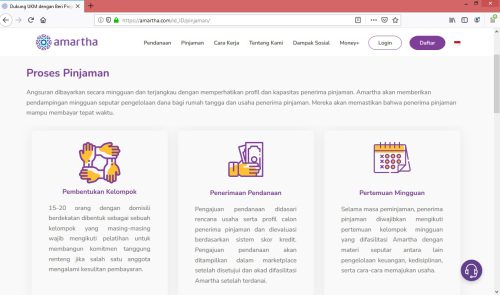

融資を受けるパートナーの場合、グループは通常、近隣の居住地に従って形成されます。このグループは15〜20人で構成できます。資金調達の提案は、事業計画と将来の融資先のプロファイルに基づいており、クレジットスコアシステムに基づいて評価されます。ローン期間中、ローンの受領者は、Amarthaが進行役を務める毎週のグループ会議に出席する必要があります。

Amarthaは、経済への女性の参加、持続可能な資金調達慣行、および金融包摂の促進を支援しています。Amarthaを通じて、村の女性起業家は仕事を続け、ビジネスを最大限に発展させることができます。

Bahasa Indonesia

Pemberdayaan Perempuan sebagai Pengusaha Mikro di Pedesaan Indonesia

Sharing Economy merupakan salah satu produk yang dihasilkan dari perkembangan teknologi informatika dan komunikasi. Masyarakat merespon positif terhadap layanan berbasis sharing economy. Sharing economy tidak hanya tentang sharing barang, kendaraan atau properti. Ada juga sharing economy yang menerapkan keuangan, termasuk pinjaman langsung antara orang dan platform yang membantu meningkatkan modal yang diperlukan untuk pengembangan ide baru di antara mereka yang berpotensi tertarik padanya.

Salah satu platform sharing economy yang menerapkan keuangan di indonesia adalah Amartha. Amartha merupakan perusahaan peer-to-peer (P2P) lending yang menghubungkan investor kepada para perempuan pelaku usaha ultra mikro dan mikro di pedesaan. Para pelaku usaha yang membutuhkan modal usaha bisa mendapatkan modal dari para investor Amartha, baik itu perorangan atau pun institusi. Investor yang meminjamkan dana akan diberikan keuntungan berdasarkan sistem credit scoring yang disediakan oleh penyedia dalam hal ini Amartha.

Amartha adalah pionir finansial teknologi (fintech) peer-to-peer lending dengan fokus pada pembiayaan modal kerja dan pemberdayaan perempuan pengusaha mikro di desa. Amartha menerapkan strategi yang mengkombinasikan kegiatan online-offline untuk menjaga produktivitas mitra Amartha di masa pandemi covid-19.

Melalui kombinasi online-offline, Amartha mengoptimalkan penggunaan teknologi seperti penyediaan berbagai inovasi produk untuk mensejahterakan mitra salah satunya melalui aplikasi A+ (Amartha Plus) yang memfasilitasi berbagai layanan seperti WarungLoan, PPOB hingga belanja borongan. Sedangkan strategi offline (lapangan) dalam memberdayakan perempuan pengusaha mikro, selain memberikan akses pendanaan Amartha juga melakukan pendampingan dan pelatihan secara rutin seperti pelatihan alternatif usaha, pelatihan literasi keuangan hingga cek kesehatan gratis.

Amartha melayani pendanaan bagi pengusaha mikro yang tidak memiliki akses layanan keuangan di pedesaan. Mitra usaha terpilih Amartha adalah pengusaha mikro perempuan dengan kebutuhan modal mulai dari Rp 1,5 juta. Proses seleksi calon penerima pinjaman dilakukan dengan algoritma skor kredit untuk menilai kelayakan berdasarkan analisa usaha dan kepribadian.

Sebagai pemilik modal yang ingin melakukan pendanaan melalui Amartha, tidak perlu khawatir karena Amartha menerapkan sistem pendanaan kelompok untuk menguatkan semangat gotong royong apabila terjadi kredit macet. Amartha telah terdaftar dan diawasi oleh Pemerintah melalui Otoritas Jasa Keuangan (OJK). Proses pendanaanpun mudah, pertama Anda membuka akun Pendana. Kemudian memilih mitra penerima pinjaman. Anda juga bisa memilih berdasar lokasi, jenis usaha, dan plafon pinjaman. Selanjutnya Anda akan mendapatkan prediksi, pembayaran pokok dan margin secara mingguan. Dana yang diterima dapat digunakan untuk mendanai kembali atau ditarik.

Untuk mitra penerima pinjaman, biasanya akan dibentuk kelompok sesuai dengan domisili berdekatan. Kelompok ini bisa terdiri dari 15-20 orang. Pengajuan pendanaan didasari rencana usaha serta profil calon penerima pinjaman dan dievaluasi berdasarkan sistem skor kredit. Selama masa peminjaman, penerima pinjaman diwajibkan mengikuti pertemuan kelompok mingguan yang difasilitasi Amartha.

Amartha mendukung partisipasi perempuan dalam perekonomian, praktik pembiayaan berkelanjutan, dan promosi inklusi keuangan. Melalui Amartha, pengusaha perempuan di desa bisa terus berkarya dan megembangkan usaha mereka secara maksimal.

English

Empowering Women as Micro-Entrepreneurs in Rural Indonesia

Sharing Economy is one of the products resulting from the development of information and communication technology. The community responded positively to sharing economy-based services. The sharing economy is not just about sharing goods, vehicles or property. There is also a sharing economy that applies finance, including direct lending between people and platforms that help raise the capital needed for the development of new ideas among those who are potentially interested in them.

One of the sharing economy platforms that implement finance in Indonesia is Amartha. Amartha is a peer-to-peer (P2P) lending company that connects investors to women ultra-micro and micro-enterprises in rural areas. Business actors who need venture capital can get capital from Amartha investors, be the individuals or institutions. Investors who lend funds will be given benefits based on the credit scoring system provided by the provider, in this case Amartha.

Amartha is a peer-to-peer lending financial technology (fintech) pioneer with a focus on working capital financing and empowering women micro entrepreneurs in villages. Amartha implements a strategy that combines online-offline activities to maintain the productivity of Amartha partners during the covid-19 pandemic.

Through a combination of online-offline, Amartha optimizes the use of technology such as providing various product innovations for the welfare of partners, one of which is through the A+ (Amartha Plus) application which facilitates various services such as Warung Loan (small shop loan) to wholesale shopping. While the offline (field) strategy in empowering women micro entrepreneurs, apart from providing access to funding, Amartha also provides regular assistance and training such as business alternative training, financial literacy training to free health checks.

Amartha provides funding for micro-entrepreneurs who do not have access to financial services in rural areas. Amartha’s selected business partners are women micro entrepreneurs with capital requirements starting from Rp. 1.5 million. The selection process for prospective loan recipients is carried out using a credit score algorithm to assess eligibility based on business and personality analysis.

As an investor who wants to do funding through Amartha, there is no need to worry because Amartha applies a group funding system to strengthen the spirit of mutual cooperation in the event of bad loans. Amartha has been registered and supervised by the Government through the Financial Services Authority (OJK). The funding process is easy, first you open a Lender account. Then choose a loan recipient partner. You can also choose based on location, type of business, and loan ceiling. Next you will get predictions, principal and margin payments on a weekly basis. Funds received can be used to refinance or withdraw.

For partners who receive loans, groups will usually be formed according to the neighboring domiciles. This group can consist of 15-20 people. Funding proposals are based on a business plan and profile of prospective loan recipients and are evaluated based on a credit score system. During the loan period, loan recipients are required to attend weekly group meetings facilitated by Amartha. Amartha supports women’s participation in the economy, sustainable financing practices, and the promotion of financial inclusion. Through Amartha, women entrepreneurs in the village can continue to work and develop their businesses to the fullest.